France moving gold from the US is reviving ghosts of the 1971 crisis and spooking global markets with fresh concerns over financial stability and dollar dominance.

France’s decision to move its last US-held gold into Paris has stirred far more anxiety than a routine central-bank portfolio adjustment normally would. The reason is simple: gold is never just gold in the global financial system. It is also a signal about trust, sovereignty, and emergency preparedness.

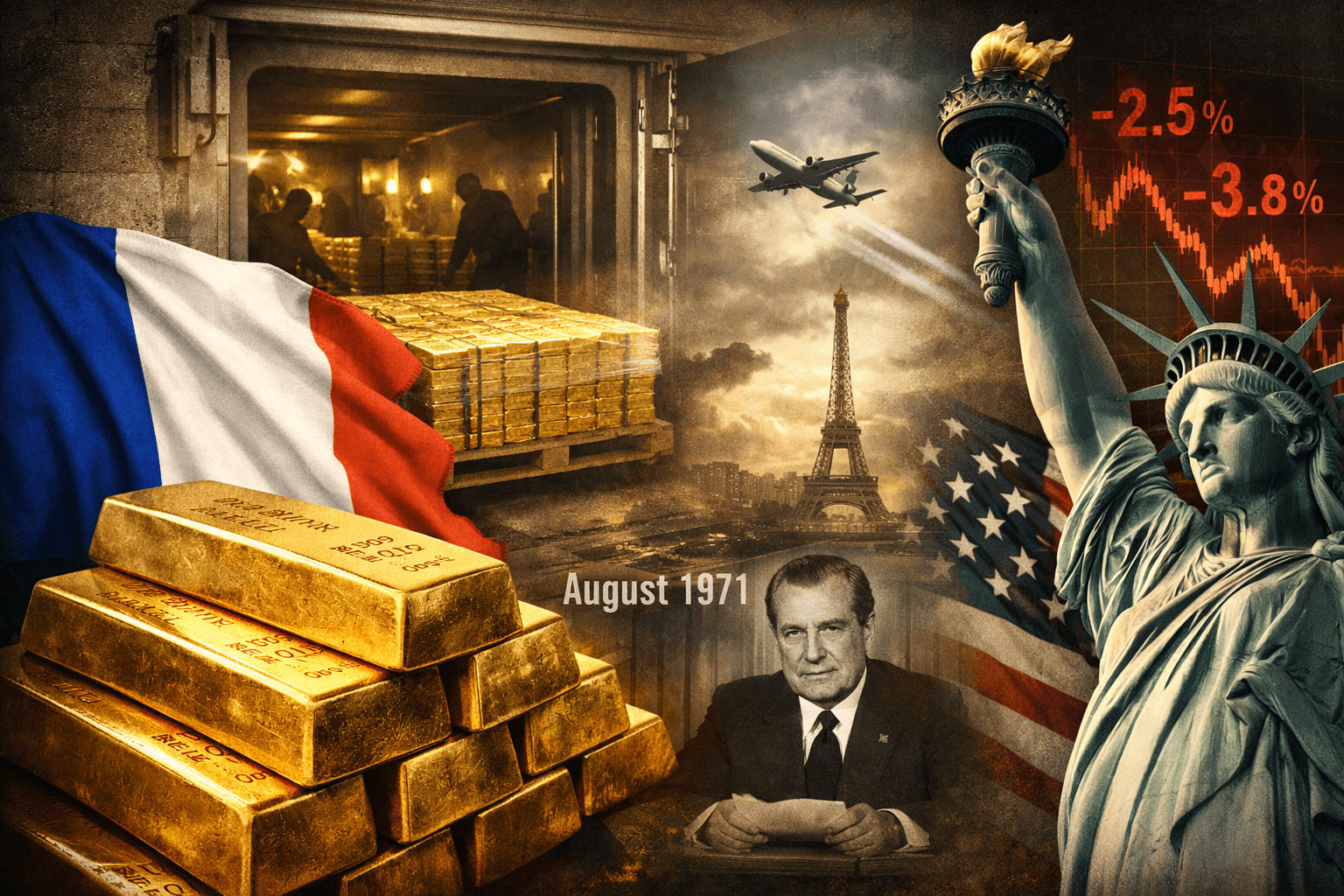

The immediate trigger for the latest debate was a Banque de France operation involving 129 metric tonnes of gold that had been held in New York. The French central bank sold older, non-standard bars at elevated market prices and replaced them with modern, compliant bars in Paris, recording a one-off gain of nearly €13 billion, or roughly $15 billion. France’s overall gold stock did not shrink; it remained about 2,437 tonnes. What changed was the form of a slice of those reserves and the place where that slice is now stored.

On paper, that sounds technical. In market psychology, however, it lands very differently. France is one of the world’s largest official gold holders. When such a country chooses to no longer keep any of its gold at the Federal Reserve Bank of New York, investors do not treat it as a mere vault-management story. They see echoes of an older moment, when French mistrust of the dollar-centered order helped expose the fragility of the Bretton Woods system and foreshadowed the 1971 collapse of gold convertibility.

That historical memory is why this story is spooking markets.

Under the Bretton Woods framework created after World War II, currencies were pegged to the US dollar, while the dollar itself was fixed to gold at $35 an ounce. Foreign governments and central banks could exchange dollars for gold, which made American monetary credibility the anchor of the postwar system. By the 1960s, however, the United States had issued far more dollars abroad than its gold position could comfortably support, and the gap between official confidence and hard-metal backing became increasingly visible.

France was one of the strongest critics of that imbalance. French officials argued that the dollar’s privileged position gave Washington an “exorbitant privilege,” allowing the US to run external deficits while the rest of the world carried the adjustment burden. During the 1960s, France pressed for a greater role for gold and increased pressure on the United States by converting dollars into bullion. That wider strain on US gold reserves contributed to the breakdown that culminated on August 15, 1971, when President Richard Nixon suspended dollar convertibility into gold, effectively closing the “gold window.”

This is why the 2026 French move feels so symbolically charged. It does not recreate the mechanics of 1971, because today’s dollar is not formally redeemable in gold. The Bretton Woods system is long gone, and no country can force the United States into a gold-settlement crisis the way foreign central banks could half a century ago. But symbolism matters. Gold repatriation by a major Western economy still raises uncomfortable questions about how central banks view geopolitical risk, counterparty dependence, and the durability of the present monetary order.

The details of the French operation are important because they also show why some of the more dramatic headlines need restraint. France did not “dump” gold, nor did it slash its reserves. According to Reuters, the Banque de France acted after a 2024 audit recommended upgrading legacy non-standard bars. Between July 2025 and January 2026, it sold 129 metric tonnes of those bars, then acquired equivalent London Good Delivery-style gold in Europe, with the replacement metal held in Paris rather than New York. Governor François Villeroy de Galhau said the choice was based on market practicality rather than politics. The bank also indicated that a further 134 tonnes of older gold already in Paris could be upgraded by 2028.

That official explanation is credible. Modern gold markets are built around standardization, liquidity, and delivery compatibility. If a central bank is holding bars that are harder to trade or use in present-day market infrastructure, switching into newer-compliant bars can make sense. Doing so when gold prices are high can also create an accounting windfall. France’s nearly €13 billion gain reflects that market backdrop rather than a reduction in bullion holdings.

Even so, markets are reacting to more than accounting. They are reacting to context.

The context is a world in which central banks have been giving more weight to reserve diversification, strategic autonomy, and sanctions resilience. Gold has regained prominence because it is a reserve asset with no issuer risk. Unlike foreign government debt, it cannot be frozen by a foreign central bank in the same way. Unlike a major reserve currency, it does not depend on the domestic politics of another state. Holding it at home can therefore be framed not only as prudent logistics but also as a layer of sovereign insurance. France has not publicly described its move in such geopolitical language, yet investors naturally read it through that lens.

Read more on Pakistan Defence Minister Kolkata Threat Draws Rajnath Singh’s 1971 Warning.

That is where the market unease comes from. If one large economy prefers all of its gold to sit on national soil, others may ask whether the assumptions behind offshore custody are shifting. The New York Fed has long served as one of the world’s premier official gold custodians. A decision by France to eliminate its remaining New York-held position does not imply distrust in the Fed itself. Still, it feeds a broader narrative that countries increasingly want direct control over hard assets in an era marked by war, sanctions, energy shocks, and strategic fragmentation.

It is also worth noting that the phrase “Ghosts of 1971” works more as a market metaphor than a literal forecast. The world is not on the verge of a replay of the Nixon shock for one key reason: the present system already operates on fiat currencies and floating exchange rates. In 1971, the crisis point was built into the architecture of the international monetary order. Today, the architecture is different. There is no formal promise that foreign-held dollars can be exchanged for US gold at a fixed price, so there is no identical pressure valve to break.

But the comparison still has power because it reminds investors of what gold movements can reveal. In the late Bretton Woods era, gold flows exposed a mismatch between financial claims and strategic confidence. In 2026, France’s move does not expose a legal contradiction in the system, but it does hint at a broader mood: major institutions still see value in hard assets, domestic custody, and optionality outside the dollar-led financial plumbing. That does not mean the dollar is about to lose reserve-currency primacy. It does mean the world’s reserve managers are showing a stronger preference for flexibility.

For investors, the bigger lesson is not that France has triggered a new monetary crisis. It is that reserve management is becoming a more politically interpreted act. In calmer times, the switch from non-standard bars in New York to compliant bars in Paris might have stayed inside central-bank balance-sheet notes. In today’s climate, it becomes a global macro story because every move involving gold is now filtered through de-dollarization fears, transatlantic uncertainty, and memories of past systemic breaks.

That is why this episode matters beyond France.

It says something about the renewed centrality of gold in official thinking. It says something about how national control over reserve assets is being valued. And it says something about market nerves: even a technically justified balance-sheet upgrade can trigger outsized reactions when trust in the international order feels less automatic than it once did.

So, is France moving gold from the US a warning sign? Yes, but not in the most alarmist sense. It is not evidence that a gold-backed world is returning, nor proof that the dollar system is about to crack. What it does show is that central banks are behaving as if resilience, convertibility, and domestic control matter more than they did in the era of easy globalization.

That alone is enough to spook markets.

Because whenever gold starts moving and France is involved, financial history has a way of speaking a little louder.