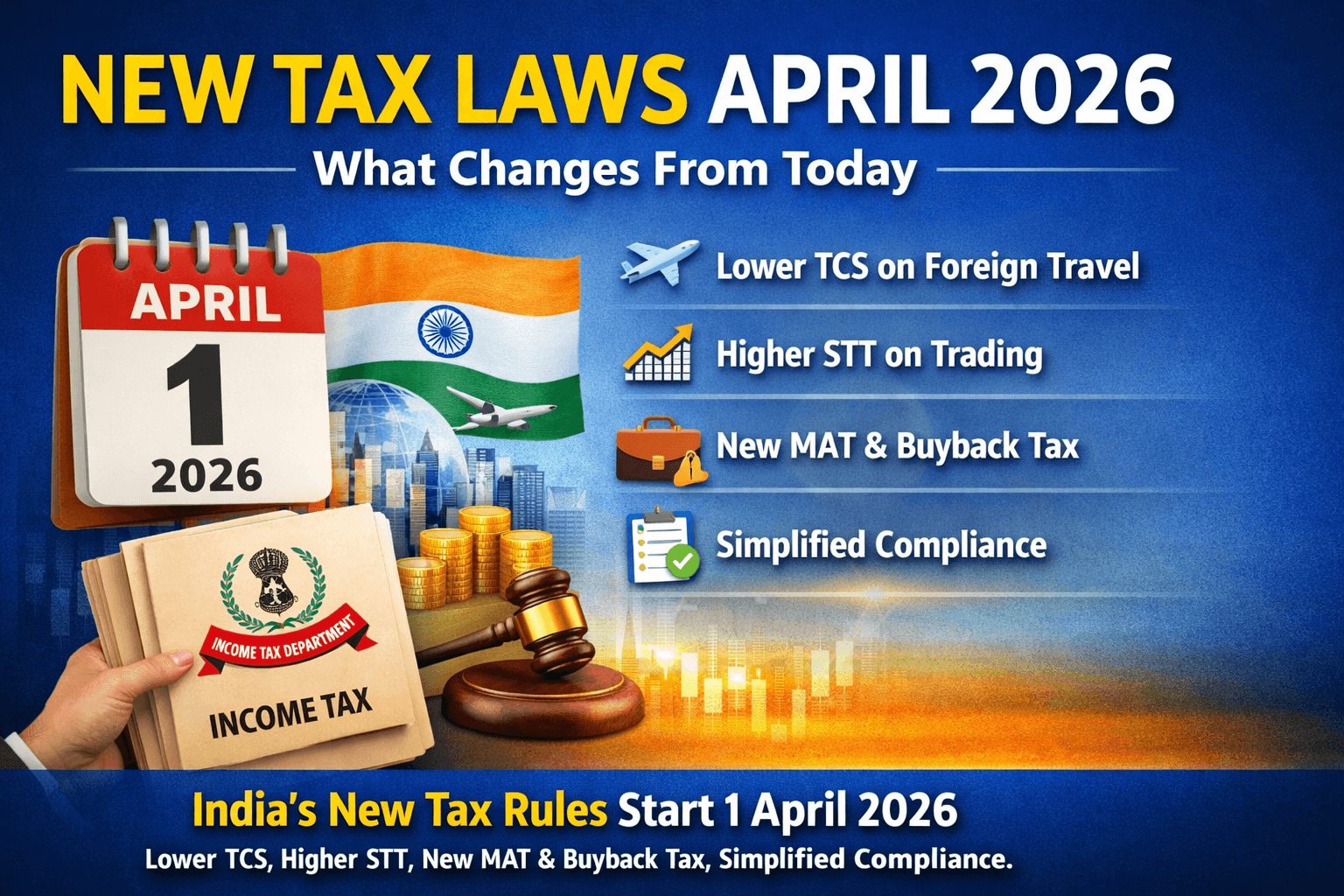

New Tax Laws April 2026: What Actually Changes From Today for Salaried Indians, Investors, Businesses and NRIs

India’s tax regime changes in a meaningful way from 1 April 2026, but the earlier version needed some tightening. The corrected picture is this: the Income-tax Act, 2025 and the Income-tax Rules, 2026 come into force from today, while the Finance Act, 2026—which received presidential assent on 30 March 2026—brings several Budget 2026 proposals into operation from today or on the dates specified in law.

The biggest headline is not a dramatic overnight slab rewrite for everyone. It is a system reset: India now moves to a simplified legal framework under the new Act, including the concept of a “Tax Year”, which replaces the old “previous year” and “assessment year” terminology for the new regime. The government has also said the law is meant to simplify language, remove obsolete provisions, and make compliance easier.

That said, today’s changes are still significant. They affect foreign travel payments, overseas remittances, F&O trading, share buybacks, corporate MAT, compensation interest in accident cases, safe harbour rules for IT services, filing timelines, and customs rules for courier and e-commerce exports.

What is the biggest change from today?

The most important change under the New Tax Laws April 2026 is the legal switchover from the Income-tax Act, 1961 to the Income-tax Act, 2025 for the new tax year beginning today. The new rules notified by CBDT also take effect from 1 April 2026.

A major simplification inside the new framework is the use of “Tax Year” as a single concept. Under the old setup, taxpayers often had to mentally separate the year in which income was earned from the year in which it was assessed. The new Act replaces that old structure with a unified “Tax Year” approach.

This is why the corrected understanding is important: today is less about one flashy single tax rate announcement and more about a broad compliance and structural transition plus a set of specific tax rule changes that now begin applying.

Relief for ordinary taxpayers: MACT interest becomes tax-free

One of the clearest taxpayer-friendly changes effective from today is on compensation awarded in motor accident cases. The Budget proposed that interest awarded by the Motor Accident Claims Tribunal (MACT) to a natural person will be exempt from income tax, and any TDS on that interest will be removed.

This matters because compensation-related payments are often received by families or individuals after distressing circumstances. Removing tax and TDS on this interest means the claimant keeps more of the awarded amount instead of facing an extra deduction at source.

TCS changes from today: foreign travel and remittances get cheaper in some cases

A major correction from the earlier summary is that the government has indeed reduced TCS on overseas tour programme packages to 2%, replacing the earlier structure of 5% and 20% depending on conditions. The Budget speech and PIB releases explicitly state this.

Similarly, under the Liberalised Remittance Scheme (LRS), the TCS rate for education and medical remittances is reduced from 5% to 2%. This is one of the more practical changes for households sending money abroad for tuition fees or healthcare.

However, the relief is not universal across all remittances. The official materials specifically highlight the reduction for education and medical treatment. So the safer, corrected reading is that taxpayers should not assume every LRS remittance now attracts only 2%; the reduction specifically applies to the categories identified in the Budget documents.

TCS on goods has also changed

Another confirmed change from today is the rationalisation of TCS on certain goods. According to official Budget releases, alcoholic liquor, scrap and minerals are rationalised to 2%, while tendu leaves are reduced from 5% to 2%.

This is important because the earlier draft article was directionally right on the 2% rationalisation, but the corrected and safest wording is to say “alcoholic liquor, scrap and minerals” rather than overstate itemised sub-categories unless the law or notification is being quoted line by line.

STT rises for futures and options traders

For market participants, one of the sharpest tax changes from today is the increase in Securities Transaction Tax (STT) in the derivatives segment. Official Budget documents say STT on futures rises to 0.05% from 0.02%, while STT on options premium and exercise of options rises to 0.15% from 0.1% and 0.125% respectively.

This makes F&O trading more expensive at the margin. For occasional traders, the increase may seem limited in isolation, but for high-frequency or high-volume derivatives participants, the higher transaction tax can add up quickly and reduce net profitability.

Share buyback tax treatment has changed

The earlier article said buybacks would now be treated as capital gains, and that point broadly stands. The official Budget releases say that buyback for all types of shareholders will be taxed as capital gains, and that promoters will bear an additional buyback tax, resulting in an effective burden of 22% for corporate promoters and 30% for non-corporate promoters.

This is a meaningful change because buyback taxation had long been debated in terms of fairness between promoters and minority shareholders. The government’s stated rationale is “in the interest of minority shareholders.”

MAT changes for companies

Another confirmed reform is around Minimum Alternate Tax (MAT). Official PIB material says MAT is proposed to become a final tax, with the rate reduced from 15% to 14%, and that further accumulation of MAT credit ends from 1 April 2026. At the same time, brought-forward MAT credit accumulated up to 31 March 2026 remains available for set-off under the new arrangement.

This is one of the more technical but significant changes for companies because it simplifies future tax treatment while preserving legacy credits already accumulated before the switchover.

Read more on Elon Musk’s Terafab & Space AI Data Centers Explained here.

NRI and foreign business-related changes

The earlier summary also mentioned incentives for non-residents and global businesses, and those points largely hold up with one important correction in wording. PIB says the Budget proposes MAT exemption for all non-residents who pay tax on a presumptive basis. It also proposes a tax holiday till 2047 for foreign companies providing cloud services globally using data centre services from India, subject to the stated framework, including service delivery to Indian customers through an Indian reseller entity.

So the corrected version should say foreign cloud providers using India-based data centre services rather than loosely saying all foreign companies using Indian data centres. The official language is narrower and more precise.

PIB also notes a safe harbour of 15% on cost where the Indian data centre service provider is a related entity.

IT safe harbour rules become more generous

For the IT services sector, the earlier article was right on the broad direction. The official record says the Budget proposes a single category of Information Technology Services with a common safe harbour margin of 15.5%, and raises the threshold for availing safe harbour from ₹300 crore to ₹2,000 crore.

This is aimed at simplifying transfer-pricing compliance and reducing friction for companies that would otherwise deal with more complicated classification and approval processes. PIB also says the safe harbour process for IT services will be handled through an automated rule-driven process.

New Tax Laws April 2026 for Salaried Individuals: A Hidden Impact Beyond Salary Slabs

Despite the absence of direct changes to income tax slabs, the New Tax Laws April 2026 represent a broader shift in India’s taxation philosophy—one that moves beyond income and begins to influence overall financial behaviour. For salaried individuals, this means that while their monthly tax outflow may remain unchanged on paper, their investment returns, international spending, and long-term wealth creation could be indirectly affected. Changes in areas such as TCS on foreign transactions, increased STT on trading, and revised taxation on share buybacks suggest that the real impact lies not in what appears on the payslip, but in how money is spent, invested, and retained over time.

Compliance and filing relief also kicks in

The corrected article should also include the compliance-side relief measures from Budget 2026. Official PIB documents say a rule-based automated process will allow small taxpayers to obtain a lower or nil deduction certificate instead of filing an application with the assessing officer.

The government also proposes to let depositories accept Form 15G and Form 15H and pass them to relevant companies, which can reduce duplication for investors holding securities in multiple companies.

Another confirmed change is that the time available for revising returns is proposed to be extended from 31 December to up to 31 March with a nominal fee. In addition, the return filing calendar is proposed to be staggered, with ITR-1 and ITR-2 individuals continuing till 31 July, while non-audit business cases or trusts are proposed to get time till 31 August.

One nuance worth keeping in mind is that the practical rollout of some return-related changes can depend on assessment-year applicability and portal implementation. Recent reporting has cautioned against assuming every deadline change applies retroactively to earlier years.

Courier and e-commerce export rules also change from today

Beyond direct tax, another “from today” reform comes from CBIC. The government has operationalised courier and e-commerce export reforms effective 1 April 2026. According to PIB, this includes removal of the ₹10 lakh value cap on courier export consignments, a Return to Origin mechanism for uncleared imports after 15 days, and simplified handling of returned or rejected imported goods.

That means today’s rule changes are not limited to income tax filers alone. Exporters, e-commerce sellers and logistics-linked businesses are also affected.

What was corrected from the earlier version?

The earlier article was broadly right on many headline points, but the corrected version sharpens the facts in four ways. First, the main story is a legal and structural transition, not merely a set of “slight tweaks.” Second, the LRS TCS reduction should be stated specifically for education and medical remittances. Third, the data-centre tax holiday applies to eligible foreign cloud service companies under the announced framework, not every foreign business with some India data-centre connection. Fourth, filing-date changes need to be described carefully because practical applicability can depend on the return year and implementation details.

Final takeaway

The New Tax Laws April 2026 mark one of the biggest tax-framework transitions India has seen in decades. From today, India is operating under the Income-tax Act, 2025 and the Income-tax Rules, 2026, while the Finance Act, 2026 activates multiple Budget 2026 changes on TCS, STT, MAT, buybacks, taxpayer relief and compliance simplification.

For salaried taxpayers, the immediate visible impact may be limited unless a specific provision touches their income or filings. But for travellers, remitters, traders, companies, investors, NRIs, IT firms, exporters and compensation claimants, the changes from 1 April 2026 are real and material.